TL;DR

- The label on the money matters less than four things you can measure.

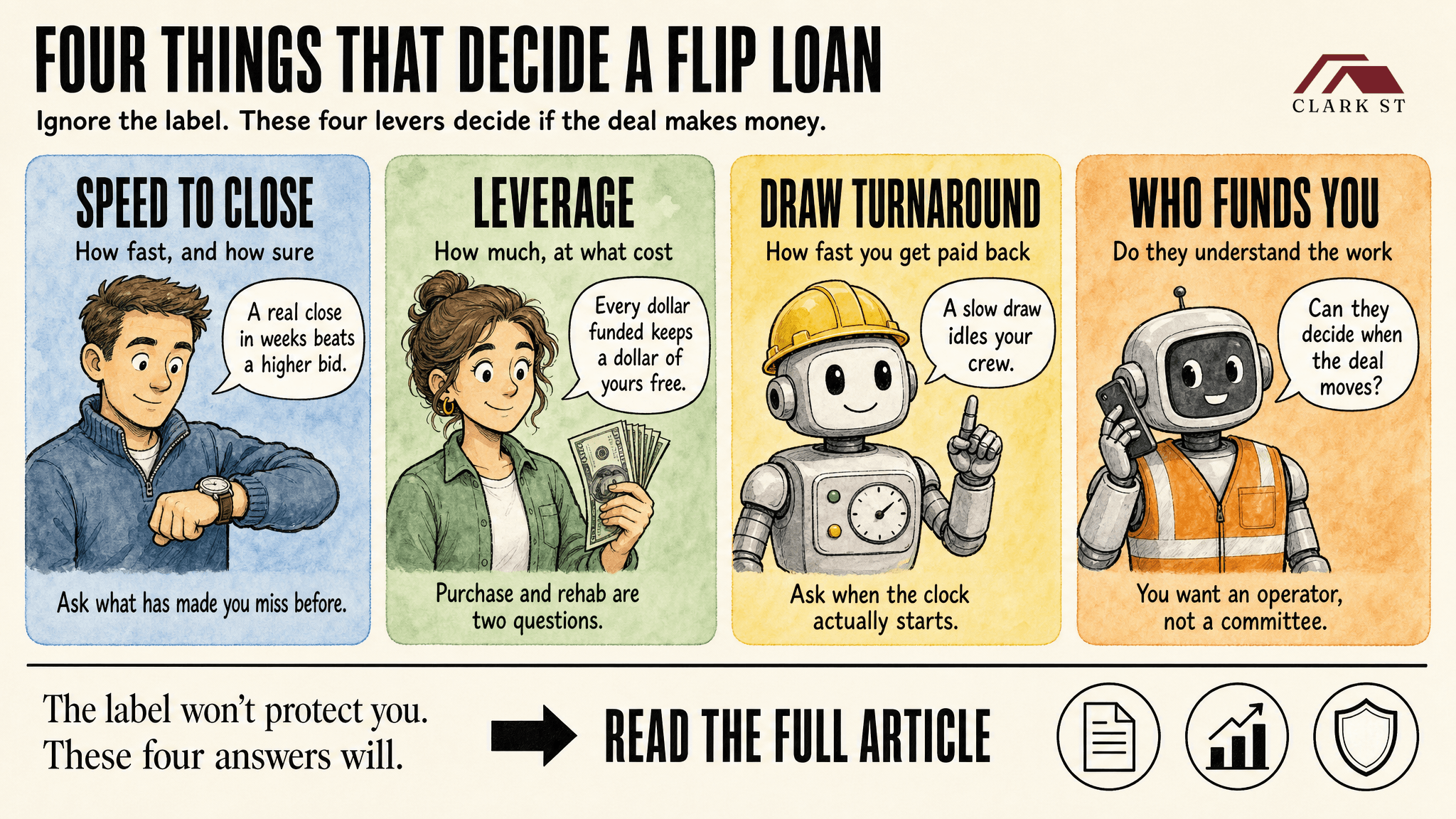

- Judge any flip loan on four levers: speed to close, leverage, draw turnaround and whether the person funding you understands the work.

- Each lever has a number you can ask for and a failure point to watch for.

- The headline rate is almost never the number that decides whether the deal makes money.

- Learn to pressure-test all four and you can size up a lender in one phone call.

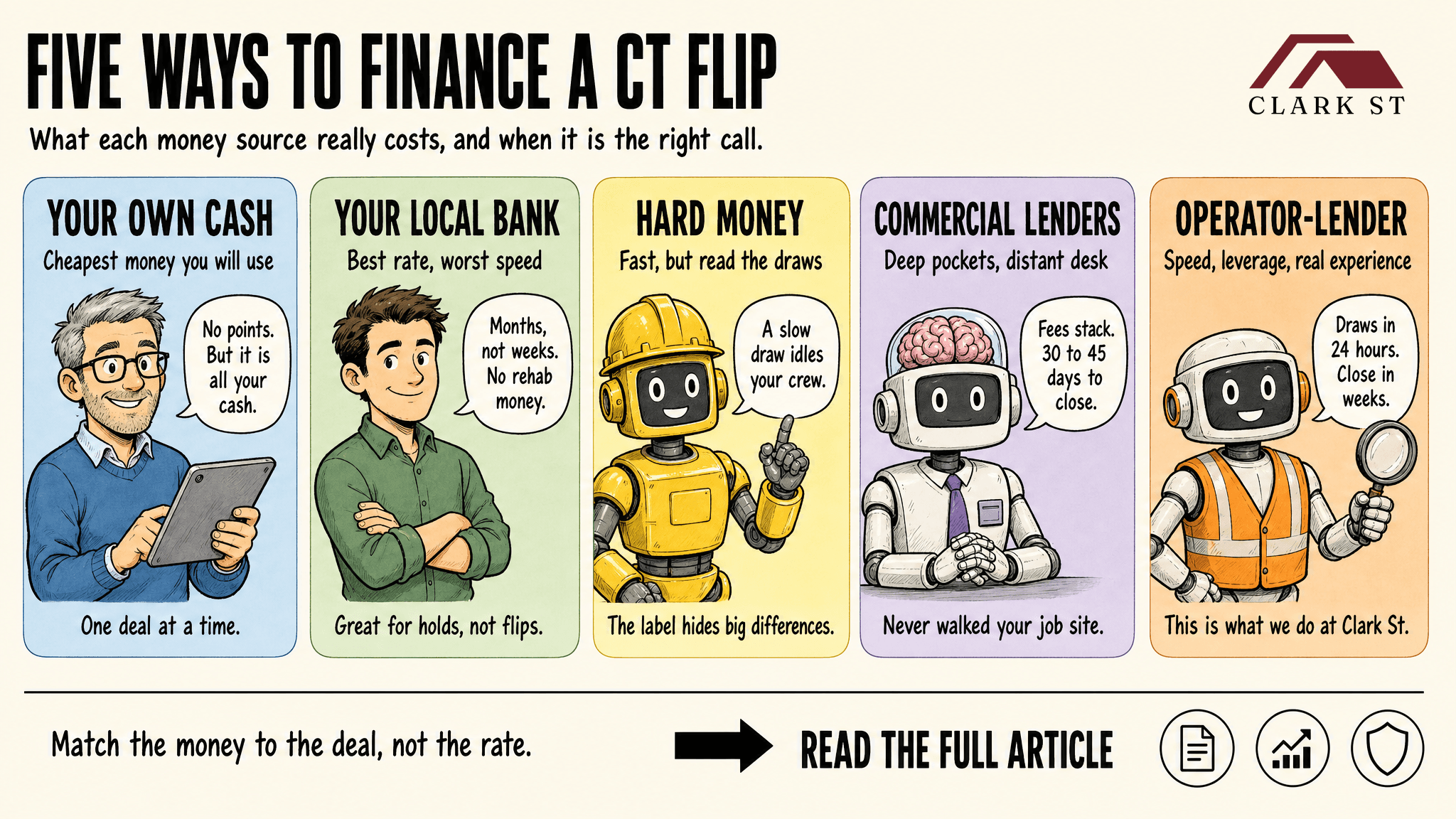

Stop shopping the label

Ask three flippers to define "hard money" and you'll get three answers. Same with "private lender." The words are loose. A private lender can be your dentist with a self-directed IRA or a national fund with a call center. The label tells you almost nothing about how the money will behave once your deal is on a clock.

So stop shopping the label. There are four things you can actually measure and every one of them decides whether your deal makes money or bleeds. Learn to ask about all four and you'll read a lender faster than any brochure ever could.

Lever 1: speed and certainty to close

The first lever is how fast the money can actually close and how sure that close is.

Here's why it matters. A motivated seller isn't only shopping price. They're shopping certainty and a timeline. The operator who can promise a real close in weeks beats a higher bidder who needs longer and comes with a contingency. And once you own the house, the clock is already running. Carrying costs, interest and market risk pile up every day between contract and close.

Different capital sources move at different speeds and the pattern is simple. The more documents and layers of approval a lender needs, the longer the close and the less certain it is. Every new request restarts the clock.

What to watch for: don't anchor on the advertised close time. Anchor on certainty. Ask two questions. What's your average close on a deal like mine? And what has made you blow past that timeline? A lender who can answer both plainly has closed deals like yours before. The one who dances around the answer is showing you a red flag.

Lever 2: leverage and what it actually costs

The second lever is how much of the deal the money will cover and what that coverage costs you.

Why it matters: leverage is really a question about your own cash. Every dollar the lender funds is a dollar of yours that stays free for the next deal or the surprise behind the wall. Rot, mold, a bad foundation sill. If your reserves are sunk in this purchase, there's nothing left to solve the problem the rehab hands you in month four.

Here's where people oversimplify. They lump two different questions into one. Question one is whether the lender funds the rehab at all. Question two is how much of the purchase and the rehab they'll fund. Those are separate. Plenty of assumptions about who funds what turn out to be wrong on the specific deal.

What to watch for: get the real numbers, not the marketing ones. How much of the purchase price? How much of the rehab? Is the rehab funded on a schedule or project milestones?

Higher leverage keeps more of your cash working and it usually costs more in rate or points. Neither is right or wrong. Know which one your deal needs and price the trade with your eyes open.

Lever 3: draw turnaround

The third lever is the one nobody asks about until it's too late. How fast the lender processes a draw.

First, how draws work, because this is where most rehab budgets get funded. You don't get the rehab money up front. You complete a stage of work, it gets verified and you get reimbursed. Then you fund the next stage. Draw speed is what keeps your crew moving and your carrying costs from eating your profits.

Why it matters: a slow draw idles your crew. When your crew stops working, they move to someone else's job and you wait to get them back. Lost time on a flip costs way more than a point on the rate ever will, when you can get predictably reimbursed and keep your project timeline on track.

What to watch for: the advertised number is rarely the real one. Plenty of lenders advertise a 24-hour draw. Read the fine print on when the clock starts. Often their clock doesn't start until a third-party inspector files a report and that inspector's turnaround is outside anyone's control, including the lender's.

So ask the mechanic questions. Who verifies the work? Is that person in-house or a third party? When does the clock actually start and what's the real process and turnaround once I submit? The honest answer to those gives you clarity beyond their marketing.

Lever 4: does the person funding you understand the work

The fourth lever is the one that decides whether the money helps you when the deal moves. It has nothing to do with the label on the loan.

Every rehab goes sideways somewhere. The plumbing is worse than the inspection showed. A permit takes an extra three weeks. A subcontractor walks. When that happens, the value of your lender is measured by three things:

Do they understand what just happened? Can they help? Can they make a decision?

Why it matters: a lender who's run rehabs reads your scope and knows real timelines from fantasy. When you say the sill was rotted, they know what that does to your timeline and your budget, because they've stood in that basement. A lender underwriting from a desk isn't a villain and distance isn't a defect. It's just a limiter. The further the decision-making sits from the job site, the more your problem has to travel before someone with authority can act on it.

What to watch for: find out who's actually on the other end. When something changes mid-rehab, who do I call? Has that person done rehabs themselves? Can they make the decision or do they have to escalate it to a manager, or worse, a committee you'll never meet? You're not looking for a friend. You're looking for someone who can understand your situation and quickly decide when a project stops going to plan.

How to pressure-test any lender

Next time someone pitches you money for a flip, ignore what they call themselves. Ask four questions and listen for specifics, not adjectives:

How fast can you actually close and what has made you miss that before? How much of the purchase and the rehab will you fund? How fast do you release a draw once the work is done and when does that clock start? When my deal changes mid-rehab, who do I talk to and can they make a decision?

The label won't protect you. These answers will. Run every lender through those four and the right money for your deal gets obvious fast.

If you've got a flip or a value-add multifamily project in Connecticut and want to see how we answer those four questions, here's how we fund deals: /borrow.

If you have any questions, I'm a cheap date. Give me a shout.

About Ed Mathews

Ed is the founder of Clark St Capital, Clark St Homes and Elevista. He started investing in 2011 after analyzing deal after deal and making zero offers, until a mentor handed him a pen and made him sign his first contract. Since then, Clark St has operated across single-family, multifamily and land development, with Ed also invested as a limited partner in funds and large multifamily projects. Ed also spent more than two decades in Silicon Valley building systems for global companies. He hosts the Real Estate Underground podcast, with new episodes every Tuesday at 12pm.