TL;DR

- Financing a flip is matching the money to the deal, the timeline and how much control you keep.

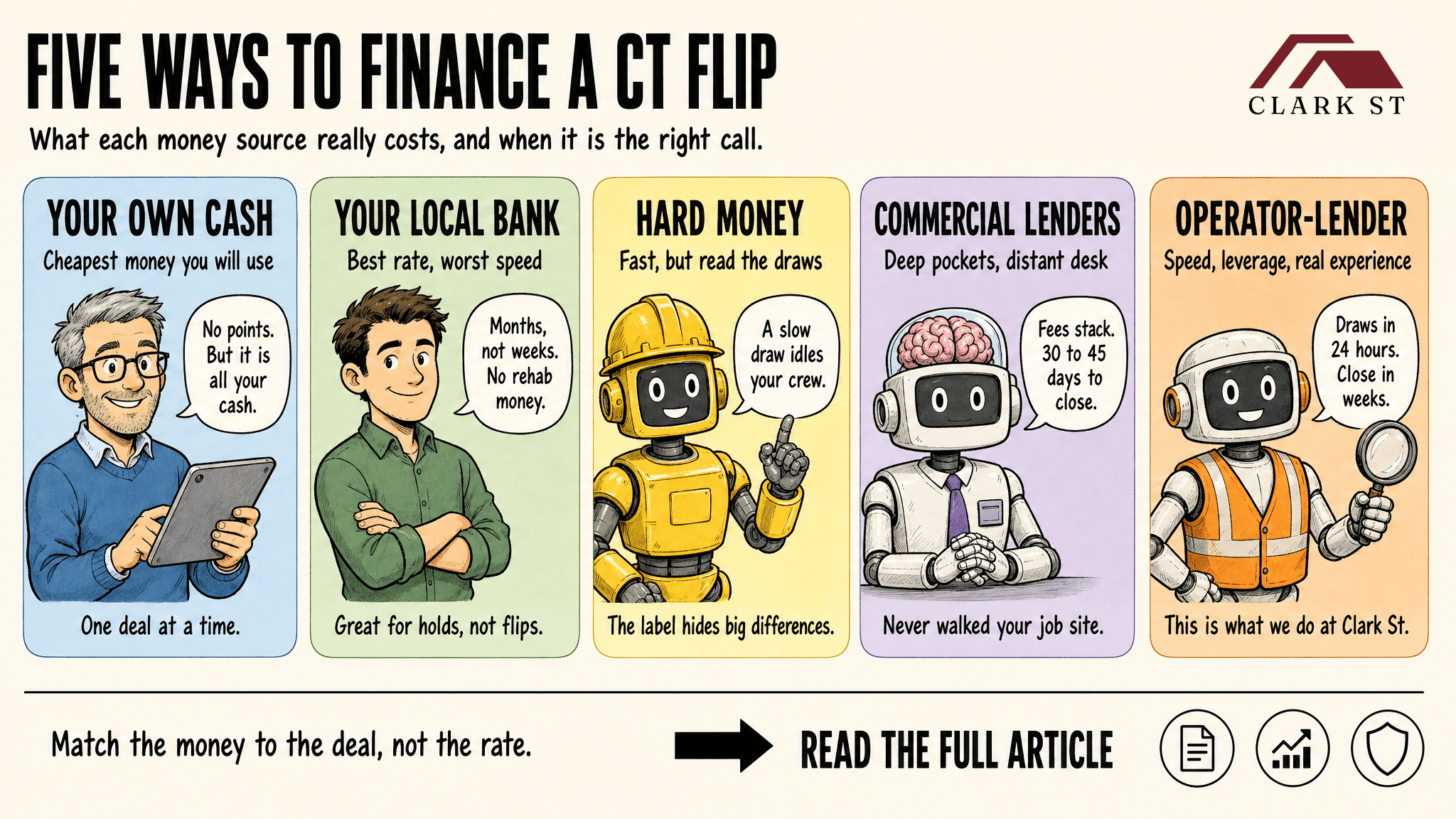

- Five ways to fund a Connecticut flip: your own cash, a bank, hard money, national commercial lenders and local, experienced operator-lenders.

- National lenders like Lima One and RCN are proven capital partners. They underwrite from a distance, so fees stack and closings run 30-45 days.

- On a flip, speed to close and draw turnaround usually cost you more than the headline rate does.

- Clark St Lending funds Connecticut 1-4 unit flips: up to $2M, up to 90% of purchase and 100% of rehab, closing in less than 30 days, usually as soon as the title clears.

Which money actually fits your flip?

The real question isn't "can I get money for this flip." You can. The decision usually revolves around the tradeoffs of speed vs rate/costs. Your seller needs speed. Your contractors need speed. You need to manage debt cost. Get any of those wrong and a good deal bleeds.

Here are the five ways Connecticut flippers actually fund a project. What each one really costs, and when each is the right call.

Your own cash

Cheapest money you'll ever use. No points, no lender, no draw process. The real cost is opportunity. Your ability to close additional deals is bound by your bank account. If you've got plenty of reserves and the deal is short-term and relatively small, use cash.

Cash in one project is cash you can't put on the next deal. And every project throws a curveball. Rot behind a wall, mold in the attic, a bad foundation sill. If your reserves are sunk in the purchase there's nothing left to solve the mid-rehab surprise.

Preserving your cash liquidity and using leverage enables you to scale your business (be careful). For most operators, that is the whole reason to bring in a lender.

Your local bank

You're going to get the best rate on paper. That's the pitch and it's real. The problem is everything else.

A bank moves at a snail's pace. Think months, not weeks. Banks underwrite your projects like a homeowner, not an operator. The paperwork needed for the underwriting process can feel like a proctology exam. Banks want the property to appraise as-is. Most banks don't care about ARV, unless you're talking to the construction department.

And it usually won't fund the rehab at all. A sub-4-unit value-add doesn't fit its box.

So the deal that needs speed is the exact deal a bank is built to pass on. Great for stabilized rentals you'll hold. Wrong tool for a flip on a clock.

Hard money

"Hard money" is a label, not a product. It covers a lot of ground.

Some hard money lenders are true operators who understand a job site. Some are pure rate-and-fee shops that have never walked a project site. Same label, very different experience. The terms and the draw process are where they help you or hurt you.

Yes. They're fast to close. But understand how draws work and the committed service levels (how fast they turn around) before you sign. A lender who sits on your draw while your crew idles will cost you more than a point on the rate ever could. Lost weeks because your crew had to move on to another project while you were waiting to get paid is a deal killer.

Commercial lenders

This is where a lot of Connecticut flippers land. These are legitimate capital sources and worth understanding.

Firms like RCN Capital, Lima One Capital, Silver Hill and others have deep pockets, and national footprints. Loans run from $50k to $5M, rates roughly 8% to 12%, with origination points tiered by experience. They'll go up to about 90% of cost and 100% of rehab. Closing runs 30 to 45 days, faster for repeat borrowers. Minimum FICO score is 660 and they want prior investment-property exits, in the last 36 months.

These are real options. We've used them before with varying success. Here's what you need to know going in.

The fees stack. Beyond points you'll see a per-draw inspection fee, commonly $100 to $250, pulled straight out of your rehab budget. Add origination, appraisal, legal, credit and background fees on top of those.

The funding decision. They're slower to decide. Underwriting tends to be strict and they can flake weeks into their process. Closings run 30 to 45 days.

Draws wait on third party inspectors. Several advertise 24-hour draw funding. But the clock doesn't start until a third-party inspector files a report. That inspector's turnaround, not the lender, is what will idle your crew.

They underwrite from a distance. Portal, third-party appraisals, third-party draw inspectors. Nobody funding the deal has walked your job site or knows the Connecticut market. And when you need help, you're reaching a junior person, not someone who can actually make a decision.

An operator-lender

The last option is money from someone who's run flips. When the person funding you has demoed buildings, installed bathrooms, chased draws and carried a job that ran long, the loan is built around how a rehab actually works.

- You're still getting leverage up to 90% of purchase and 100% of rehab, so your own cash stays free.

- You're closing in weeks, so your seller gets their problem solved quickly.

- Your draws are funded in 24 hours or less, so your contractors can focus on the project, not on the money.

These lenders understand your scope without waiting on an outside inspector. Many use AI-assisted technology to enable you to request draws on-site from your phone with a few simple pictures.

This is what we do at Clark St. Connecticut-based projects focused on:

- Single family flips and small value-add multifamilies (2-4 units)

- Up to $2M, up to 90% of acquisition and 100% of rehab

- Draws in 24 hours or less

- Closing in weeks, typically in less than 30 days

- 12 months of interest-only at 10% to 15% plus 3 points

- 660 minimum credit and a 6-month interest reserve

When you need help, you're dealing with one of our principals, not an employee.

We don't do ground-up or 5-plus units yet. If that's your deal, we're not the right fit.

Honest tradeoff: an operator-lender isn't the cheapest rate on the street. A bank wins on rate. What you're buying is speed, leverage and a lender who's done the work.

On most flips that's the trade-off that helps you grow.

How to actually choose

Match the money to the deal. Don't shop rate first. Ask three questions:

- How fast do I need to close and how certain does that close need to be?

- How much of my own cash do I want tied up in this one deal?

- If a draw or a timeline slips, does this lender have room built in to keep me solvent?

The headline rate is the number everyone anchors on. It's rarely the number that decides the profitability of the deal. Carrying costs run every day, whether contractors are working or not. A lost deal due to underwriting delays costs way more than any points will.

On a flip, speed, experience and leverage usually beat a cheaper rate.

If you have a Connecticut flip or a small value-add multifamily deal and want to see what an operator-lender's terms look like, here's how we fund deals: /borrow.

If you have any questions, I'm a cheap date. Give me a shout.

About Ed Mathews

Ed is the founder of Clark St Capital, Clark St Homes and Elevista. He started investing in 2011 after analyzing deal after deal and making zero offers, until a mentor handed him a pen and made him sign his first contract. Since then, Clark St has operated across single-family, multifamily and land development, with Ed also invested as a limited partner in funds and large multifamily projects. Ed also spent more than two decades in Silicon Valley building systems for global companies. He hosts the Real Estate Underground podcast, with new episodes every Tuesday at 12pm.