TL;DR

- The commercial real estate maturity wall is roughly $2.0 trillion of commercial and multifamily debt that has been maturing from early 2025 and will continue through 2027, into higher rates and lower values. About 37% of it was originated when fed funds sat below 0.25%, now 3.63%.

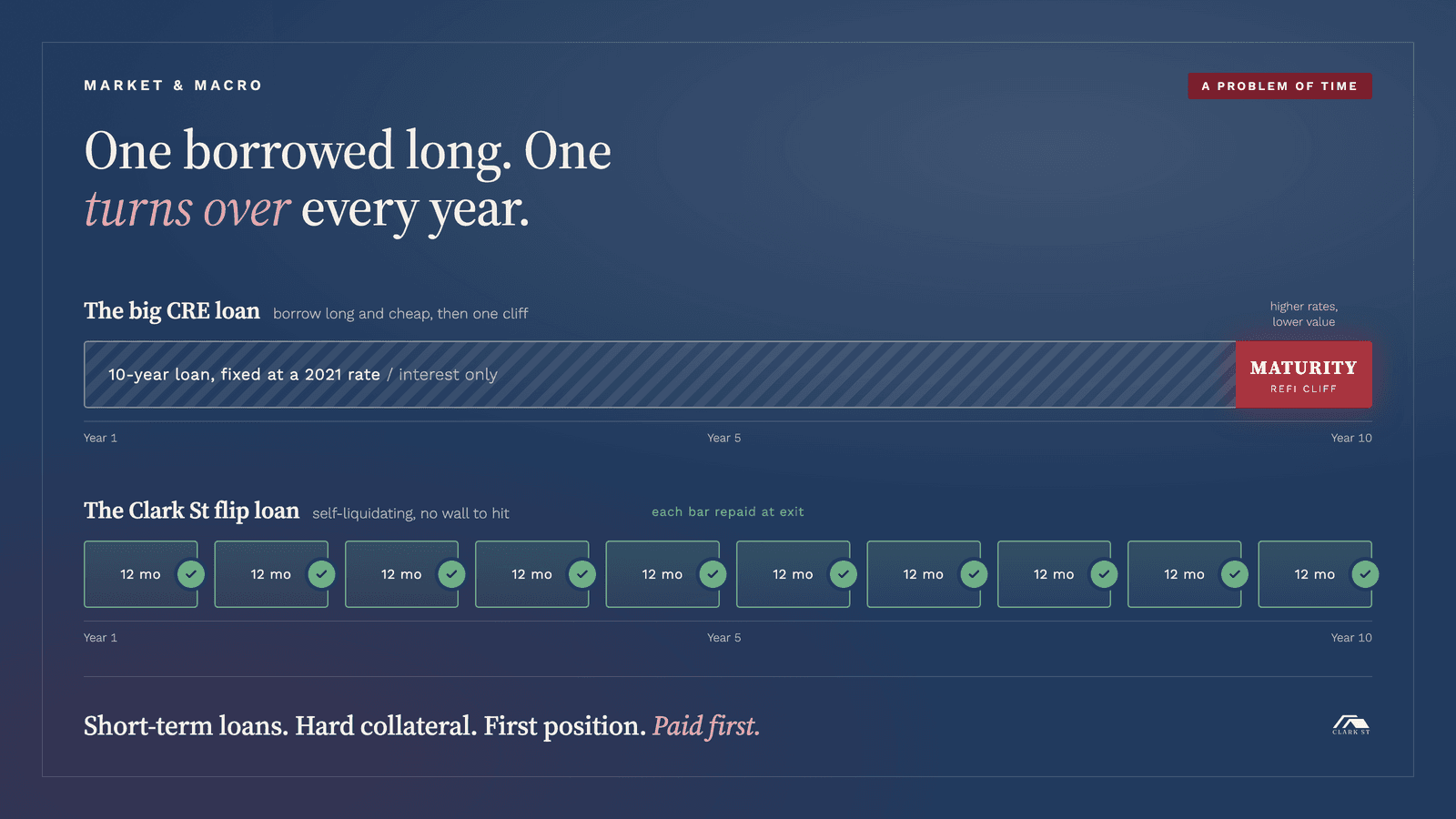

- It exists because big owners borrowed long and cheap against peak prices and now can't refinance at par. It's a problem of time.

- A 12-month fix-and-flip loan is self-liquidating, so there's no refi cliff. US 1-4 unit housing is about 88.6% fixed long-term debt.

- We're not immune. A high-rate, soft market reaches us through the borrower's exit, not through a maturity cliff.

- The real defense is underwriting discipline: conservative loan-to-value, ARV haircuts, a real equity cushion and first position.

What is the commercial real estate maturity wall and why can't owners just refinance?

Big commercial owners borrowed long and cheap against peak valuations. Those loans now mature into a higher-rate, lower-value world, so the new loan won't cover the old payoff. Roughly $2.0 trillion of commercial and multifamily debt has been maturing from early 2025 and will continue through 2027, according to Newmark. About 37% of it was written when the fed funds rate was under 0.25%. That rate is now 3.63%. The Mortgage Bankers Association puts the single-year load at about $875 billion due in 2026 alone. That's the wall.

The other half of the problem is the collateral. The building backing a maturing loan is worth less than it was when the loan was written. There are two clean reasons why.

The first is cap-rate expansion. Value equals net operating income divided by the cap rate. When rates rise, cap rates rise with them, which mechanically drops the value of the same income. Move a property from a 5% cap to a 6% cap and you've cut its value by roughly 17% without changing a dollar of income. That's just the math of the denominator getting bigger.

The second is that the income itself missed pro forma. The deals also bet on a calm that never showed up. Most 2021-2022 offering memorandums assumed inflation would hold at 2 to 3 percent and rents would climb 5 percent or more every year, indefinitely. Neither held. Inflation ran above 3 percent for roughly three straight years, from April 2021 through mid-2024. It peaked at 9.1 percent in June 2022, the highest in four decades, against a Federal Reserve target of 2 percent. We're not an island. Pandemic-era stimulus, snarled supply chains and the 2022 energy shock from the war in Ukraine pushed up the cost of fuel, materials and everything that moves on rail, a truck or ship. Those costs land on a property's expense line: insurance, taxes, payroll, debt service. So expenses climbed while the 5 percent rent growth reversed. Asking rents spiked about 17 percent in early 2022, then fell back toward and below the long-run norm of 3 to 4 percent. The income that was supposed to outrun costs came in under pro forma from both directions.

Apartments are down about 20% from their July 2022 peak, per MSCI's RCA index, while industrial sits at new highs. Office is the epicenter, down roughly 50% from its March 2022 peak with CMBS delinquency at an all-time high near 11.66% in August 2025, per Trepp. Everyone already knows office is broken.

Why is the maturity wall really a problem of time?

The pain is the mismatch. A long-term loan at a fixed low rate is resetting into a higher-rate, lower-value world. The owner is stuck holding an asset they can't refinance at par and can't easily sell without crystallizing the loss. The clock ran out on a bet that needed the old environment to stay put.

When the new senior loan won't cover the old payoff, something has to fill the gap. That's where mezzanine debt and preferred equity step in. They sit above the senior loan and below the common equity, bridge the shortfall and price high because they're taking the risk the senior lender won't. It keeps the deal alive. It doesn't make the owner whole. It eats into whatever return was left.

Strip it down and the disease is duration. The maturity wall is a problem of time. The fix for a problem of time is to not have any.

Why isn't a short-term residential debt fund exposed to the maturity wall?

A 12-month fix-and-flip loan is self-liquidating. It gets repaid at the exit, when the operator sells or refinances the finished property. It never gets rolled for years. The loans turn over constantly, so there's no wall to hit. The maturity wall is a problem of time. Short-term debt removes the time.

The structure backs this up. US residential 1-4 unit debt is about 88.6% fixed-rate long-term debt, per FHFA Working Paper 24-03 on the lock-in effect. Homeowners hold onto low fixed loans, so there's no maturity wall on that collateral. Compare that to the short balloon structures across commercial real estate that must refinance on a schedule no matter what rates are doing. Different debt, different risk entirely.

Then there's the collateral we choose. We lend against Connecticut single-family and small multifamily. Connecticut behaves like a low-volatility asset. In the 2008 crash, Connecticut home prices fell about 20% peak-to-trough on the FHFA index. Florida fell 45%, Arizona 46%, Nevada 56% on that same index. The Sunbelt cratered. Connecticut bent. Part of that is supply: about 1 in 10 Connecticut homes were built since 2000, third-lowest in the country, which puts a floor under value because you can't flood the market with new construction. Through 2025 Q2, FHFA had Connecticut up 7.8% year over year against roughly 2 to 3 percent nationally. Steady collateral, not a moonshot.

This is the answer to why we fund Connecticut flips instead of big apartment deals. Short-term loans on a low-volatility asset is a different business than long-term loans on a market that has to cooperate.

So is a short-term debt fund immune to high rates? No. Here's where they reach us.

We don't carry refi-cliff risk. We're not immune to the rate environment either. Any operator who tells you otherwise is selling something.

A high-rate, soft market makes the borrower's exit harder. The operator may have to sell below the projected after-rehab value. Or they can't refinance into the debt-service coverage the model assumed. The deal that pencils at one set of rates stops penciling at another. That pressure comes back to the fund as default and extension risk, not as a maturity cliff. The risk is real. It lives at the borrower's exit, not in the structure of our loans.

So the honest answer is not a wall in our portfolio. It's the exit getting tougher on the other side of the table. Which is exactly why the answer is discipline, not a claim of immunity.

How do we protect capital when the rate environment is stacked against the borrower?

The defense is in how we underwrite every loan.

We lend below 70% of the projected after-rehab value. Capping the loan under 70% of finished value builds a 30%-plus equity cushion beneath us. Even if the exit comes in under projection or the market softens, the collateral still covers the loan. That's the concrete protection against the exact downside above. It holds together with our terms to the operator, up to 90% of acquisition and 100% of rehab, because that's loan-to-cost. Add it up and the total loan still lands under 70% of finished value.

The rest of the discipline stacks on top. We haircut ARV and underwrite to a discounted exit, not the borrower's optimistic one. We require a real equity cushion, so price has to fall through the borrower's money before it ever reaches ours. We hold first position, paid before borrower equity sees a dollar. We lend against value an operator can force through the rehab, not a market we hope cooperates.

Our debt fund targets 11% or better. That's a target, not a guarantee. It's paired with the structure above for a reason. The structure is what makes the target credible.

The maturity wall is a story about borrowing long against assets you can't control. The Clark St Capital Preservation Fund does the opposite. Short-term loans. Hard collateral. First position. Paid first.

Want the operator's read on the credit market?

I send the same lessons I would give a friend over coffee, the stories and the math behind the deals, in the Clark St Underground Insights newsletter. No hype, no pitch, just how an operator thinks about protecting and deploying capital through a cycle like this one. If you want to understand the structure instead of being sold a pitch, join the list.

New episodes of Real Estate Underground drop every Tuesday at 12pm. Subscribe wherever you get your podcasts.

About Ed Mathews

Ed is the founder of Clark St Capital, Clark St Homes and Elevista. He started investing in 2011 after three years stuck in analysis paralysis, running the numbers on deal after deal without making a single offer, until a mentor pushed him to sign his first contract. He's forever grateful she did. Since then, Clark St has operated across single-family, multifamily and land development, with Ed also invested as a limited partner in funds and large multifamily projects. Ed also spent more than two decades in Silicon Valley building systems for global companies. He hosts the Real Estate Underground podcast, with new episodes every Tuesday at 12pm.