A real estate syndication and a real estate debt fund both get sold the same way: "invest in real estate." But they sit on opposite sides of the same deal. A syndication buys the equity and owns the upside and the downside. A debt fund lends against the property and gets paid first, before any equity sees a dollar. One is built to chase a number. The other is built to protect one. Which seat fits you depends less on the pitch and more on where you are in your own financial journey.

TL;DR

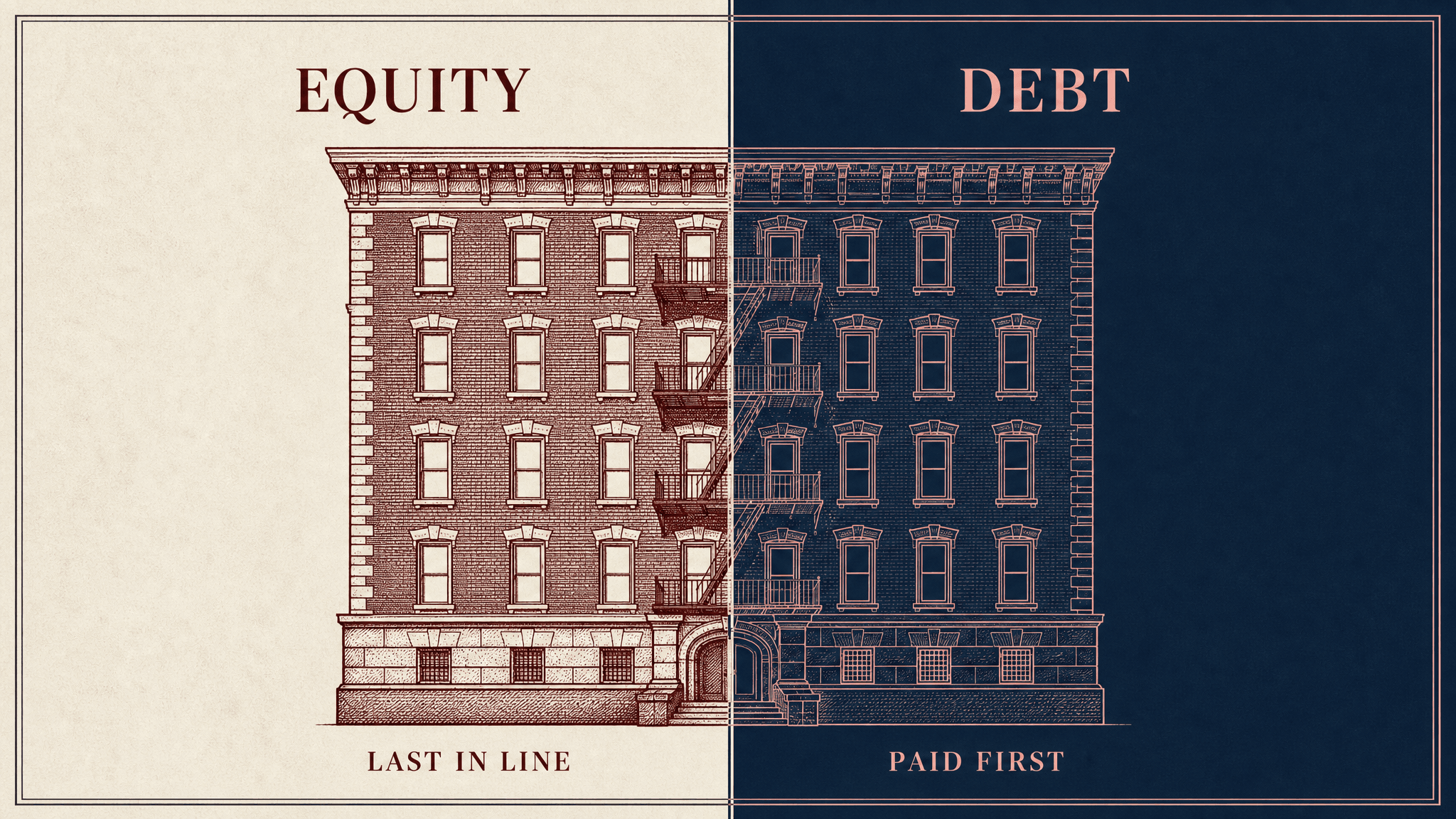

- A syndication buys the equity. A debt fund lends against the property. Same building, opposite ends of the capital stack.

- Position in the capital stack is the whole game. Debt gets paid first. Equity absorbs the first loss.

- Where you are in your financial journey usually decides which end fits. Building wealth points toward equity's upside. Protecting it points toward the lender's seat.

- The multifamily blowups of the last three years happened on the equity side. Lenders still got paid.

- When we lend, we require a personal guarantee. That is just one of the protections an agency non-recourse loan doesn't have.

Same building, opposite ends of the stack

Picture one property and two investors.

The first buys in as an owner. They're in the equity. If the property appreciates, refinances well and sells for more than it cost, they win. If it doesn't, they're the ones who take the loss.

The second doesn't own anything. They lend money against that same property and hold a lien on it. They collect interest and they get paid before the equity collects a dollar of profit.

That order isn't trivial. Debt sits in first position, closest to the asset. Equity sits behind. When money comes in, debt gets paid first. When money runs short, equity gets wiped out first. The owner's equity is the cushion that has to disappear before the lender feels any pain. Same address. Very different risk.

Which end fits you depends on where you are

There is no universally correct seat. There is a seat that fits you.

If you are early and building, hunting growth and you can stomach a market swing, equity's upside may be exactly what you want. That's a real strategy and it's a good one.

If you've already built something and your job now is to keep it, the risk tolerance and math flips. You don't need the home run. You need reliable income and a floor under your capital. You want singles and doubles.

That's the lender's seat. Most of the accredited investors we talk to are in this second group. They're executives, business owners, doctors and attorneys who earned it once and have no interest in learning real estate the hard way to earn it again.

The blowups happened on the equity side

You've heard the multifamily stories from the last three years. Big syndications that raised on IRR projections of 18% - 20%.

Many did very well, a few hit the wall.

Rate caps expired. Values dropped. The refinance those plans depended on never arrived. Capital calls went out and a lot of investors either wrote another check or watched their equity go to zero.

Almost all of that pain landed on the equity. The lenders on those same deals largely got paid.

The lenders who didn't were mostly agency non-recourse loans. Non-recourse means the lender's only claim is the property itself. When the building's value fell below the loan, they had nothing else to pursue. They took the asset and ate the difference.

That's a structural weakness and it's one we don't accept. When we lend, we require a personal guarantee from the borrower. If the collateral ever falls short, we aren't limited to the building. We have recourse to the operator who signed for the loan. That is a second layer of downside protection an agency non-recourse loan simply doesn't have and it's one of the reasons the lender's seat, structured this way, holds up when a cycle turns.

Where the return comes from

The return on the debt side isn't a bet on a sale years out. It comes from interest the borrower pays, the points collected at origination and the equity cushion beneath the loan. Our debt fund targets an eleven percent return to investors. That is a target, not a guarantee and it's built to be steady rather than spectacular.

The tradeoff is real. Equity pays more when everything goes right and loses more when it doesn't. Debt gives up the top of the upside in exchange for getting paid first. That is not a lesser bet. It is a different one, for a different job.

The choice isn't which one pays more. It is which seat matches where you are on your financial journey and how much risk you want to carry. If you've decided your job now is to protect what you've built, the lender's seat deserves a serious look.

Want the operator's view on how these structures behave in a real cycle, told through actual deals instead of projections? That is what our newsletter, Underground Insights, talks about monthly. It's not tips and tricks. It's real deals and actual lessons we've learned putting capital to work and protecting it.

Sign up at clarkst.com/newsletter.

Prefer to listen? Subscribe to the Real Estate Underground podcast for the same conversations, unscripted.